It could be argued that uncertainty has been the biggest hurdle of 2023 for businesses around the globe. Economic turbulence due to the lasting effects of the COVID pandemic paired with geo-political disruptions has created an environment of uncertainty that both clients and candidates alike are feeling.

These external factors have impacted decision-making processes for both employers and executive candidates, and we’ve seen the market shift away from being heavily candidate-driven. However, in our practice we also continue to see candidates prioritising culture and compensation as they view new opportunities while clients are evaluating their leadership needs holistically to ensure alignment and growth.

Organisations are working to overcome hurdles and are looking seriously at talent as an opportunity to bridge skill gaps and better meet customer needs. K&R clients are thinking deeply about strategies for attracting and developing talent in addition to succession planning:

In our most recent survey, nearly two-thirds of our respondents expressed they did not have reservations about recruiting leadership from outside their industry, something we’re seeing in practice this year. Responses from across the food-value chain highlighted the need for stronger assessment and development programs within their organisations as well as more robust succession planning efforts.

These survey responses highlight the need for trusted leadership and talent advisors in organisations of all sizes and stages. In addition to immense functional expertise and a deep knowledge of your industry, those advisors also bring the ability to view unique business challenges through the broad lens of talent and leadership providing targeted guidance to accelerate an organisation’s growth.

The AESC Global Conference underscored the transformative role of Artificial Intelligence (AI) in shaping our future economies and leaders. The advent of generative AI, particularly large language models like OpenAI’s ChatGPT, heralds a new era of innovation. These models excel in creating content comparable to human efforts and promise significant productivity gains across various domains, including coding and customer engagement.

Despite its prowess, AI presents challenges such as ‘hallucinations’—producing plausible but inaccurate content—and inherent biases, necessitating rigorous oversight. Upcoming EU regulations and US executive orders foreshadow a tighter governance landscape, emphasizing the high-risk nature of AI applications in areas like human resources.

Leadership in the AI epoch demands a paradigm shift—curiosity, creativity, and a propensity for investigation and experimentation will be as vital as technical knowledge. The need for adaptability extends beyond CEOs to all senior executives, who must navigate AI’s implications actively.

At Kincannon & Reed, we view AI as a valuable adjunct in executive search, useful for tasks like research and candidate documentation, but not a replacement for the nuanced executive and industry expertise of human consultants. AI’s limitations in understanding organisational culture and emotional intelligence highlight the irreplaceable role of human judgement in executive recruitment. Despite AI’s potential for automation, its greatest value lies in enhancing, not replacing, the deep expertise and discerning judgement of executive search professionals, a principle central to our firm’s approach.

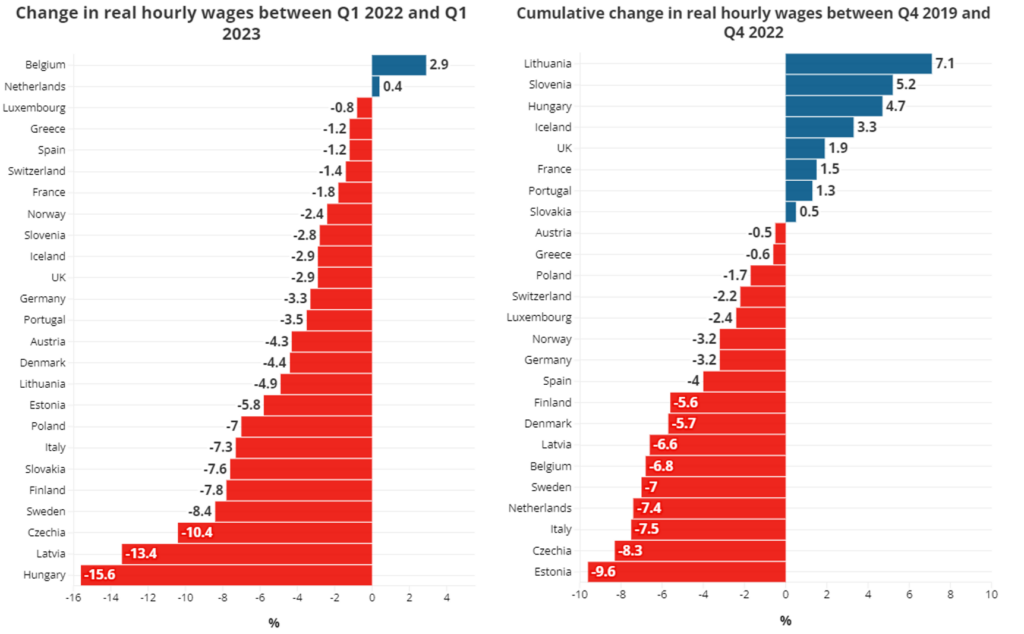

Recent OECD data indicates a decrease in real hourly wages across several European countries, with France seeing a 1.8% drop, the UK 2.9%, and Germany 3.3%, between Q1 2022 and Q1 2023. This contrasts with an upward trend in Belgium, where real hourly wages rose by 2.9%, and the Netherlands, with a modest increase of 0.4%. Such shifts reflect the nuanced dynamics of the labor market across these nations.

This shift is further validated in our own data, with compensation rates leveling out rather than continuing their climb as they had the past two years. Anecdotally, we’re seeing: